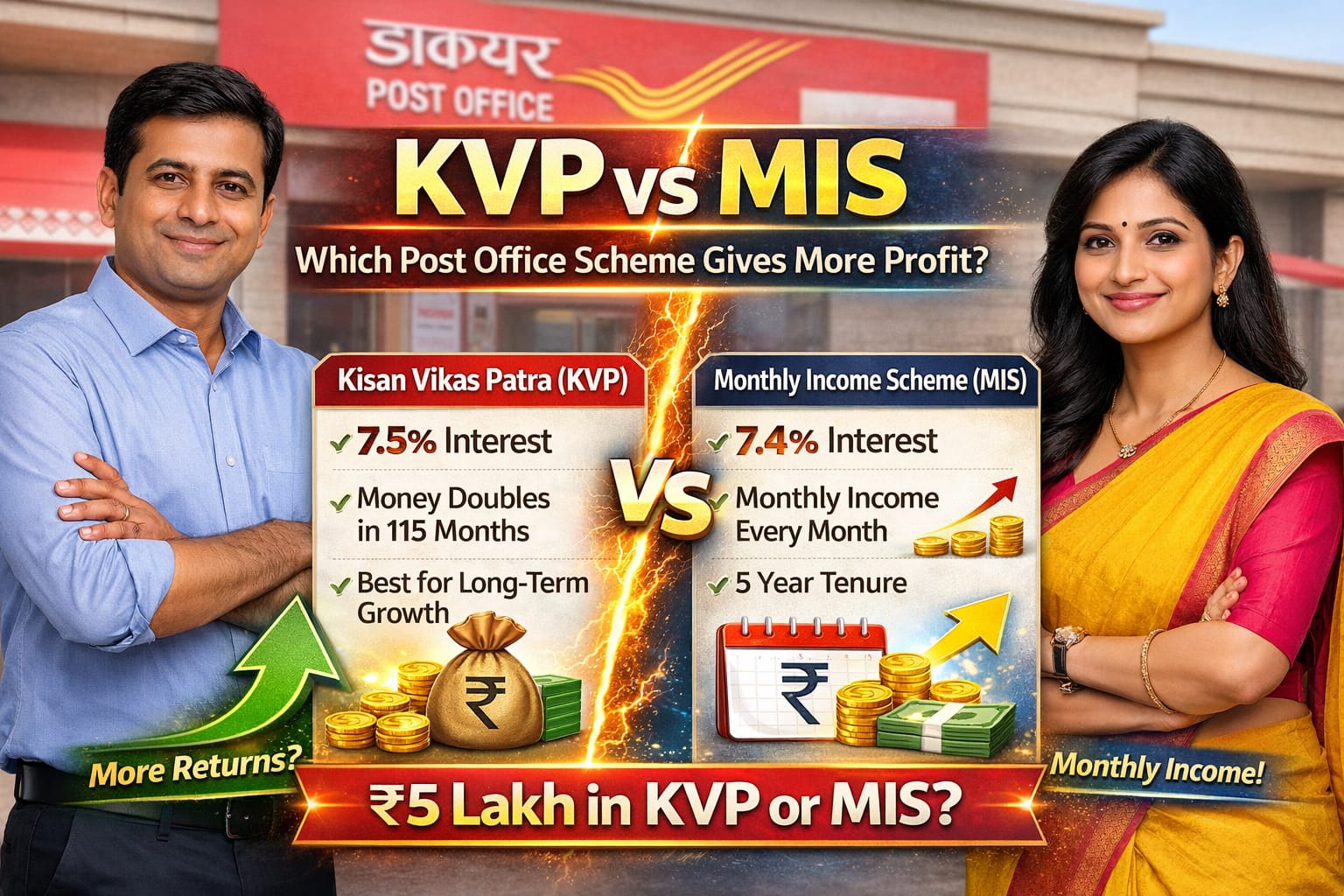

भारत में अगर कोई व्यक्ति safe investment + guaranteed return चाहता है, तो Post Office की schemes सबसे पहले दिमाग में आती हैं। इनमें दो schemes सबसे ज्यादा popular हैं:

- Kisan Vikas Patra (KVP)

- Post Office Monthly Income Scheme (MIS)

लेकिन असली confusion यहीं से शुरू होता है👇

👉 “कौन सी scheme ज्यादा फायदा देगी?”

👉 “किसमें पैसा invest करना सही रहेगा?”

👉 “Growth बेहतर है या monthly income?”

इस article में हम दोनों schemes को basic नहीं बल्कि deep level पर समझेंगे — ताकि आप बिल्कुल clear decision ले सकें।

📌 Kisan Vikas Patra (KVP) – Detailed समझ

Kisan Vikas Patra

KVP एक ऐसी scheme है जिसमें आपका पैसा एक निश्चित समय में double हो जाता है।

👉 यह scheme उन लोगों के लिए बनाई गई है जो:

- long-term investment करना चाहते हैं

- risk नहीं लेना चाहते

- guaranteed growth चाहते हैं

🔍 KVP कैसे काम करता है? (Deep Logic)

KVP में interest compound basis पर yearly add होता है। इसका मतलब:

- हर साल interest आपके principal में जुड़ता है

- अगले साल interest नए amount पर लगता है

👉 यही compounding effect आपके पैसे को double करता है

💰 KVP Interest और Maturity Calculation

मान लो आपने ₹1,00,000 invest किया:

- Interest Rate: ~7.5%

- Maturity Time: ~115 महीने

👉 Final Amount ≈ ₹2,00,000

👉 लेकिन यहाँ important बात:

आपको बीच में कोई income नहीं मिलती, पूरा पैसा end में मिलता है

KVP की खूबियां – Advanced View

✔️ Wealth Creation Tool

यह scheme wealth grow करने के लिए best है

✔️ No Maximum Limit

आप unlimited पैसा invest कर सकते हैं

✔️ Safe & Govt Backed

100% secure

⚠️ KVP की सीमाएं

- liquidity कम है

- regular income नहीं मिलती

- inflation risk हो सकता है

📌 Monthly Income Scheme (MIS) – Deep समझ

Post Office Monthly Income Scheme

MIS एक ऐसी scheme है जिसमें आपको हर महीने fixed income (interest) मिलता है।

👉 यह scheme उन लोगों के लिए best है जिन्हें:

- passive income चाहिए

- stable cash flow चाहिए

- risk-free income चाहिए

🔍 MIS कैसे काम करता है?

MIS में interest monthly payout के रूप में दिया जाता है।

👉 Example:

- आपने ₹5 लाख invest किया

- Interest rate: ~7.4%

👉 Monthly income ≈ ₹3,000+

MIS का पूरा Calculation समझें

- Annual Interest = ₹5,00,000 × 7.4% = ₹37,000

- Monthly Income ≈ ₹3,083

👉 यानी हर महीने fixed income

MIS की खूबियां

✔️ Regular Income

हर महीने पैसा मिलता है

✔️ Ideal for Retired People

pension जैसा income

✔️ Stable Return

market fluctuation का असर नहीं

⚠️ MIS की सीमाएं

- growth कम है

- investment limit है

- inflation impact हो सकता है

KVP vs MIS – Deep Comparison

🔹 1. Investment Philosophy

👉 KVP = Growth mindset

👉 MIS = Income mindset

👉 अगर आप wealth build करना चाहते हैं → KVP

👉 अगर cash flow चाहिए → MIS

🔹 2. Time Value of Money

👉 KVP में:

- पैसा block रहता है

- long-term benefit मिलता है

👉 MIS में:

- पैसा धीरे-धीरे वापस मिलता है

- immediate benefit मिलता है

🔹 3. Cash Flow Analysis

👉 KVP:

- Zero cash flow

- final lump sum

👉 MIS:

- Regular monthly income

- fixed cash flow

🔹 4. Risk vs Reward

दोनों schemes safe हैं, लेकिन:

- KVP → long-term risk (inflation)

- MIS → low growth risk

🔹 5. Inflation Impact

👉 KVP में:

- long-term inflation impact हो सकता है

👉 MIS में:

- monthly income inflation से कम हो सकती है

₹5 लाख का KVP vs MIS Return – Complete Calculation

📊 पहले समझ लो logic

👉 KVP में:

- पैसा एक साथ grow होता है (compound)

- maturity पर double amount मिलता है

👉 MIS में:

- पैसा grow नहीं होता

- हर महीने interest income मिलती है

📌 ₹5 लाख KVP Calculation – Detail

👉 Investment: ₹5,00,000

👉 Interest Rate: ~7.5%

👉 Time: ~115 महीने

👉 Final Amount ≈ ₹10,00,000

📊 KVP Growth Table (Approx)

| Year | Amount (Approx) |

|---|---|

| 1 Year | ₹5,37,500 |

| 3 Year | ₹6,20,000 |

| 5 Year | ₹7,20,000 |

| 7 Year | ₹8,40,000 |

| 9.5 Year (Maturity) | ₹10,00,000 |

👉 मतलब:

₹5 लाख → ₹10 लाख (double)

📌 ₹5 लाख MIS Calculation – Detail

👉 Investment: ₹5,00,000

👉 Interest Rate: ~7.4%

👉 Annual Interest = ₹37,000

👉 Monthly Income ≈ ₹3,083

Real Scenario Analysis

🧑 Scenario 1: Young Investor

👉 Goal: पैसा बढ़ाना

👉 Strategy: KVP

👨👩👧 Scenario 2: Family Person

👉 Goal: monthly expenses manage करना

👉 Strategy: MIS

👴 Scenario 3: Retired Person

👉 Goal: regular income

👉 Strategy: MIS

💡 Hybrid Strategy – Best Approach

👉 सबसे smart तरीका:

✔️ 50% KVP + 50% MIS

👉 फायदा:

- growth भी मिलेगा

- income भी मिलेगी

Advanced Comparison Table

| Factor | KVP | MIS |

|---|---|---|

| Return Type | Double money | Monthly income |

| Liquidity | Low | Medium |

| Best For | Long-term | Short-term income |

| Growth | High | Medium |

Taxation Deep Analysis

👉 दोनों schemes में:

- interest taxable है

- TDS नहीं कटता

👉 मतलब:

आपको खुद tax file करना पड़ेगा

Common Mistakes

❌ सिर्फ interest देखकर decision लेना

❌ goal define न करना

❌ long-term planning ignore करना

Expert Investment Tips

✔️ diversify करें

✔️ long-term सोचें

✔️ जरूरत के हिसाब से invest करें

Final Decision Logic

👉 अगर आपका goal है:

- पैसा grow करना → KVP

- income कमाना → MIS

👉 Final verdict:

KVP = Future wealth

MIS = Present income

Final Conclusion – Deep Insight

KVP और MIS दोनों ही शानदार schemes हैं, लेकिन इनका purpose अलग है।

👉 KVP आपको financially strong बनाता है (future में)

👉 MIS आपको financially stable रखता है (present में)

👉 सबसे best तरीका है:

दोनों का combination use करना