आज के समय में retirement planning बहुत जरूरी हो गई है। अगर आप हर महीने सिर्फ ₹2000 invest करते हैं, तो भी आप future में एक अच्छा pension बना सकते हैं — इसके लिए NPS (National Pension System) एक powerful option है।

NPS (Full Form) क्या है?

NPS का पूरा नाम है – National Pension System

यह भारत सरकार द्वारा शुरू किया गया एक retirement saving scheme है, जिसे Pension Fund Regulatory and Development Authority (PFRDA) regulate करता है।

👉 इसका main goal है:

- retirement के बाद regular income (pension) देना

- long-term wealth creation

NPS के Key Features

- ✔️ Low cost investment plan

- ✔️ Market linked returns (Equity + Debt)

- ✔️ Compounding का powerful benefit

- ✔️ Flexible investment (₹500 से शुरू)

- ✔️ Partial withdrawal facility

- ✔️ Retirement पर lump sum + pension

Eligibility (कौन NPS खोल सकता है?)

- उम्र: 18 से 70 साल

- Indian citizen (Resident / NRI)

- KYC documents required

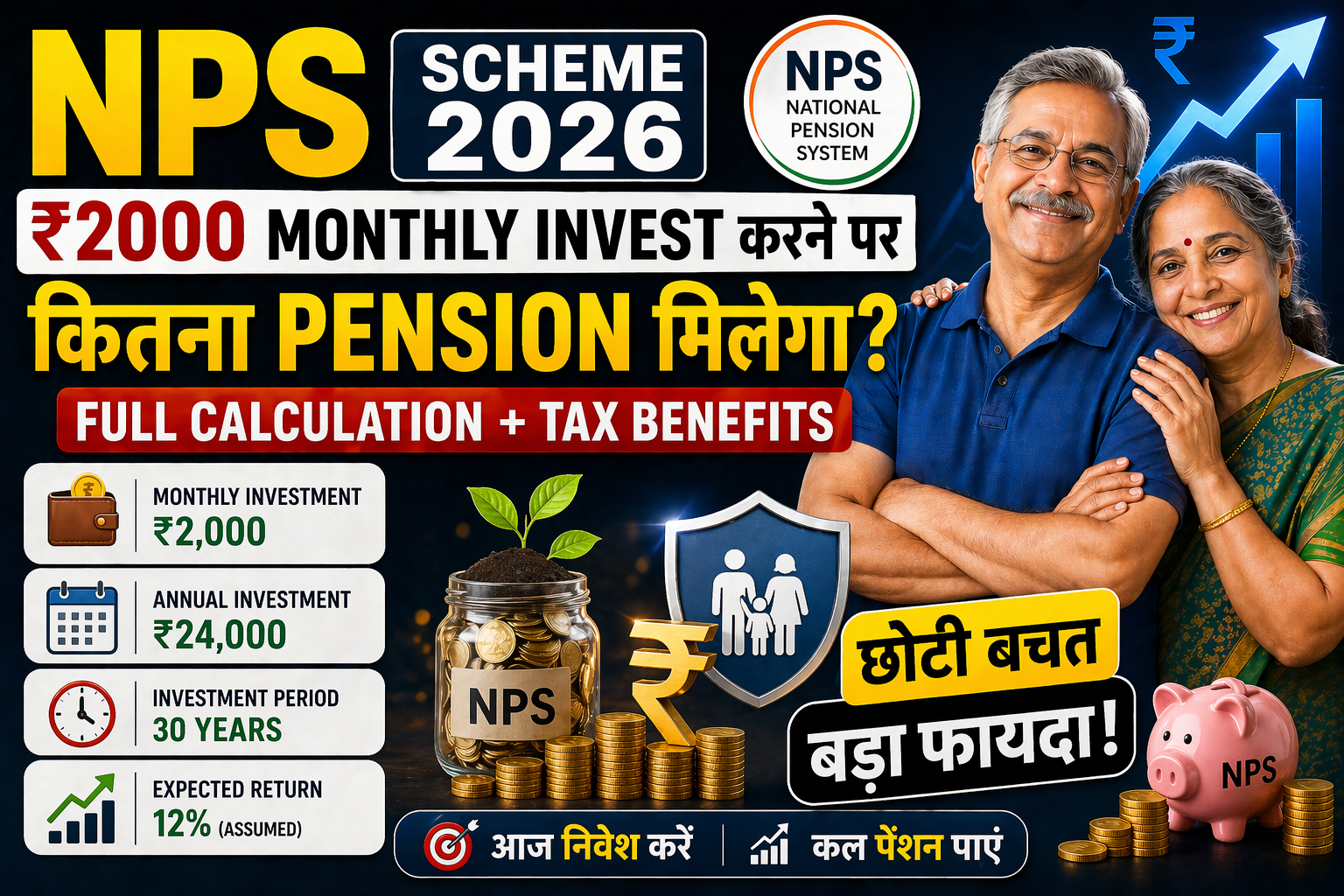

₹2000 Monthly Investment – Full Calculation

मान लेते हैं:

- Monthly investment = ₹2000

- Annual return = 10% (average)

- Time = 30 साल

👉 Formula (Compound Growth)

FV = P \times \frac{(1+r)^n – 1}{r}

Investment Growth Table (Approx)

| Year | Total Invested | Estimated Value |

|---|---|---|

| 5 | ₹1,20,000 | ₹1,55,000 |

| 10 | ₹2,40,000 | ₹4,10,000 |

| 15 | ₹3,60,000 | ₹8,35,000 |

| 20 | ₹4,80,000 | ₹15,20,000 |

| 25 | ₹6,00,000 | ₹26,50,000 |

| 30 | ₹7,20,000 | ₹45,00,000 |

👉 Total Investment = ₹7.2 लाख

👉 Final Corpus ≈ ₹45 लाख

Retirement पर क्या मिलेगा?

NPS rules के अनुसार:

- 60% = Lump Sum (tax free)

- 40% = Pension (Annuity में जाता है)

👉 Calculation:

- Lump Sum (60%) = ₹27 लाख

- Pension Fund (40%) = ₹18 लाख

Monthly Pension कितना मिलेगा?

अगर annuity return ~6% मानें:

- ₹18 लाख × 6% = ₹1,08,000 yearly

- 👉 Monthly Pension ≈ ₹9,000 / month

Breakdown (Simple समझें)

- ₹2000/month → ₹45 लाख corpus

- ₹27 लाख → एक साथ मिलेगा

- ₹18 लाख → pension बनेगा

- ₹9000/month → lifetime income

NPS Tax Benefits

- Section 80C → ₹1.5 लाख तक

- Section 80CCD(1B) → extra ₹50,000

- Total benefit = ₹2 लाख deduction

👉 Employer contribution पर भी extra benefit मिलता है (80CCD(2))

NPS vs PPF vs SIP

| Feature | NPS | PPF | SIP (Mutual Fund) |

|---|---|---|---|

| Return | 8–12% | ~7% | 10–15% |

| Risk | Medium | Low | Medium-High |

| Lock-in | 60 age | 15 years | No lock-in |

| Pension | Yes | No | No |

| Tax Benefit | High | High | Limited |

👉 Conclusion:

- Safe = PPF

- Growth = SIP

- Pension = NPS

NPS के फायदे

- ✔️ Guaranteed pension system

- ✔️ Tax saving + wealth creation

- ✔️ Long-term compounding

- ✔️ Government regulated (safe)

NPS के नुकसान

- ❌ पैसा 60 साल तक lock रहता है

- ❌ Market risk (returns fixed नहीं)

- ❌ Pension rates कम हो सकते हैं

- ❌ Full withdrawal allowed नहीं

NPS Account कैसे खोलें?

आप 2 तरीके से खोल सकते हैं:

Online:

- NSDL e-Governance Infrastructure

- Karvy Fintech

Offline:

- Bank या post office जाकर

👉 Required:

- Aadhaar

- PAN

- Bank account

- Mobile number

Conclusion

अगर आप अभी से ₹2000/month invest करते हैं, तो retirement तक एक अच्छा corpus बना सकते हैं और ₹9000/month pension पा सकते हैं।

👉 NPS उन लोगों के लिए best है जो:

- Long-term planning करना चाहते हैं

- Tax बचाना चाहते हैं

- Retirement secure करना चाहते हैं

Disclaimer

यह आर्टिकल केवल educational purpose के लिए है। NPS returns market-based होते हैं, इसलिए actual returns अलग हो सकते हैं। निवेश करने से पहले financial advisor से सलाह जरूर लें।